BELGIUM TAX REFORM

Introduction of a Capital Gain Tax as of January 1, 2026

The Belgian federal government has foreseen an important reform of the Income Tax Code 1992 (CIR92), which introduces a specific taxation on capital gains from financial assets by individuals (tax residents of Belgium).

1. Introduction of a general tax rate of 10%

As of January 1, 2026 Belgium introduces a new tax of 10% that applies to capital gains on financial assets such as shares and bonds (including cryptocurrencies and some insurances), realized by individuals as part of the “normal management” of their private wealth.

Taxation applies to individuals, provided their portfolio management remains “normal.”

However, speculative activities or those similar to professional management may fall outside the scope of “normal” private wealth management and thus not benefit from the reduced 10% tax rate, instead being subject to heavier taxation (33% as miscellaneous income or up to 50% as professional income).

2. Base exemption for small investors

A base exemption of 10.000 euro/year has been foreseen for every individual tax payer (+ 1.000 euro/year for the successive 5 years under certain conditions). This aims to protect small investors.

3. Deductibility of losses

Capital losses will be deductible from the realized capital gains, provided they relate to the same category of assets and occur within the same tax year.

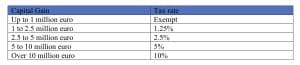

4. Regime for substantial shareholdings (>20%)

Sales of shareholdings exceeding 20% (“substantial interest”) are exempted until 1 million euro and subject to progressive taxation as follows above 1 million:

5. Exit Tax in case of Transfer of Tax Residence

It is specified that certain events will be treated as a disposal for consideration within the meaning of Article 90, paragraph 1, 9° of the Belgian Income Tax Code 1992 (CIR92), and will therefore be subject to the new 10% capital gains tax.

By consequence, the transfer of tax residence or of the seat of fortune outside of Belgium, is aimed in order to prevent the untaxed relocation of latent capital gains.

This provision thus introduces, de facto, a form of “exit tax” for individuals. This means that even without an actual sale, a Belgian tax resident could be taxed on unrealized capital gains at the time of their departure from Belgium. Please note however that some exceptions (deferral of the tax) have been foreseen in the event of relocation within the EU or a country with which Belgium has signed a double tax treaty. If the taxpayer does not realize the capital gain within 24 moths after departure from Belgium, no exit tax will be due in principle.

6. Entry into force

The date of entry into force is January 1, 2026. This means that the new capital gain tax will apply to capital gains on financial assets realized as of January 1, 2026.

The text of law provides for asset valuation as of December 31, 2025, as a reference point for calculating future capital gains. For individuals who become a Belgian tax resident from 2026 onwards, the market value of their financial assets on the date of their arrival will be considered as the acquisition value.

In principle individuals will need to declare themselves the realized capital gains in their personal income tax return in Belgium (as of income year 2026).

Please note that, on the date of drafting of this memorandum, the final legislative text has not been published yet in the Belgian Official Gazette.

Do not hesitate to contact us if you have any questions regarding this new capital gain tax, the application of it and filing via the personal income tax return.

With kind regards,

An De Reymaeker – International Tax Lawyer

an.dereymaeker@vandendijk-taxlaw.be

Vandendijk & Partners – Tax Lawyers

February 20, 20